What Every Woman Needs to Know About Inheritance Tax

It was once a tax on the very wealthy. Frozen thresholds, rising asset values, and a landmark change to pension rules arriving in April 2027 have quietly made it something else entirely.

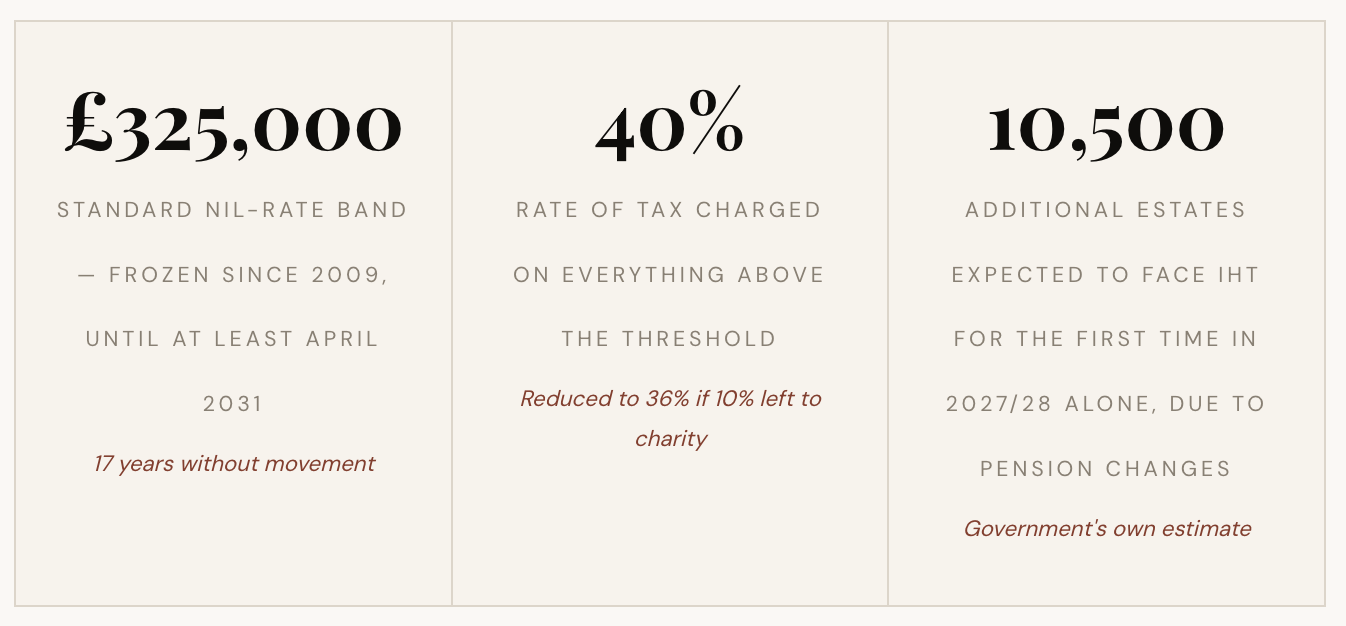

There is a number that has not changed since April 2009. Seventeen years of rising house prices, growing investment portfolios, and expanding pension pots, and the basic threshold at which inheritance tax becomes payable has remained precisely where it was: £325,000. In the same period, the average UK house price has risen from around £155,000 to over £290,000. The maths is not complicated. What was once a tax that touched roughly three percent of estates now catches closer to six percent, and the Office for Budget Responsibility projects that figure will keep rising every year through to 2030.

Inheritance tax is no longer a problem that belongs exclusively to the wealthy. It is increasingly a problem that belongs to anyone who owns a home in a city, has been saving into a pension for two decades, and has watched their investments grow. And from April 2027, it will become significantly more complex, as unused pension pots are brought into the taxable estate for the first time.

The planning window is not infinite. Some of the most effective strategies require years to mature. This guide sets out what the rules are, what is changing, and what you can do now.

How Inheritance Tax Works

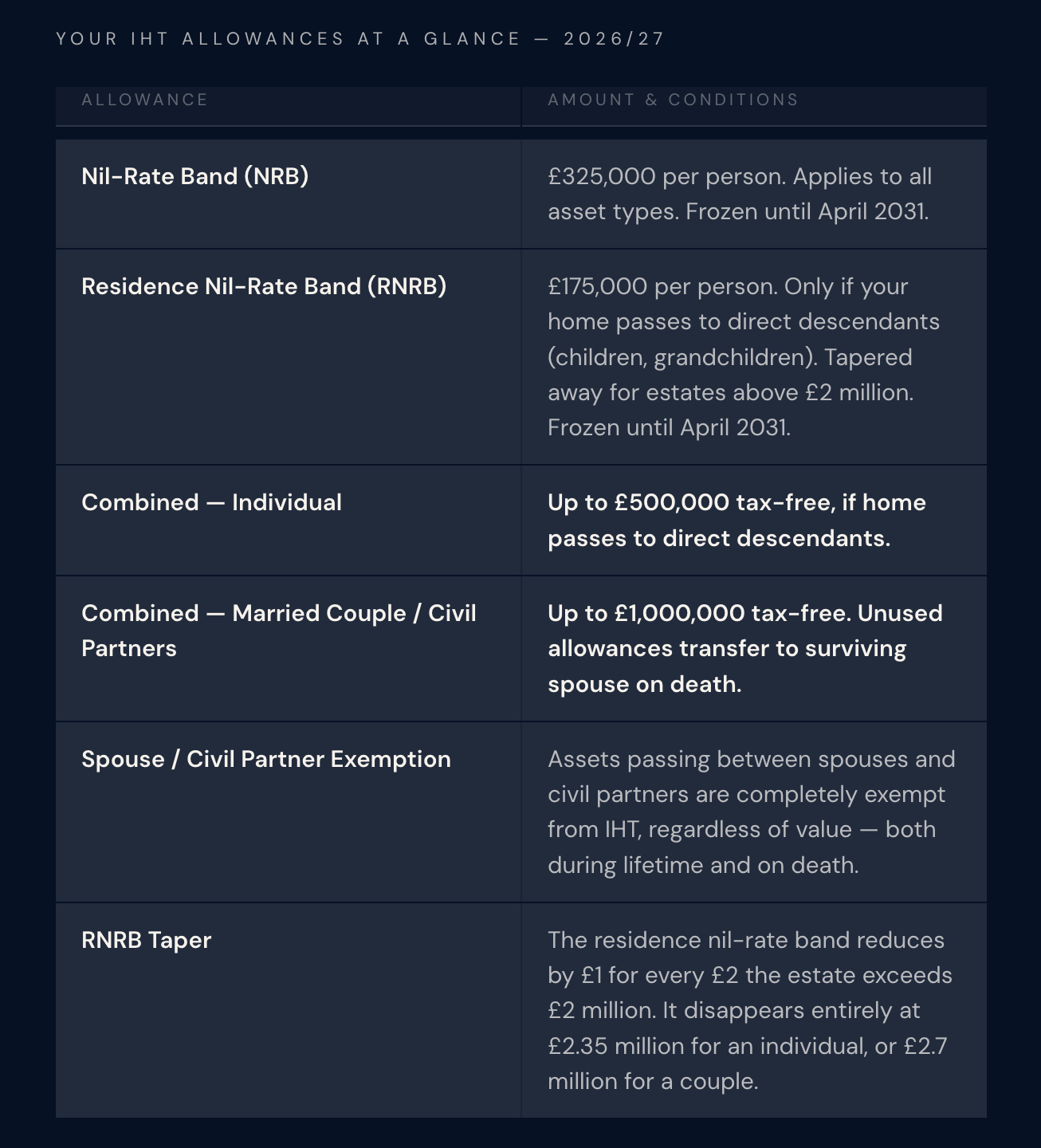

All figures current for 2026/27. All thresholds confirmed frozen until April 2031. Source: HMRC / Finance Act 2025.

When you die, everything you own is added together. Your home, savings, investments, jewellery, art, ISAs… all of it. This total, minus any debts and funeral costs, is your estate. If its value exceeds your available allowances, the portion above the threshold is taxed at forty percent. The tax must generally be paid before probate is granted, which can create genuine liquidity challenges for families whose wealth is tied up in property.

The rate itself has not changed. What has changed is how many people find themselves subject to it, as the frozen thresholds fail to keep pace with rising asset values. This is fiscal drag in its purest form: the government collects more revenue each year without technically raising the rate.

Who is Actually Affected

The short answer is: more people than most assume, and the number is growing every year. The RNRB was introduced in 2017 specifically to protect family homes, and it did provide meaningful relief for many estates. But it comes with conditions that trip people up. It only applies if you pass your home to a direct descendant, so those without children, those who leave their home to a sibling or other relative, or those whose estates exceed the £2 million taper threshold may not benefit from it at all.

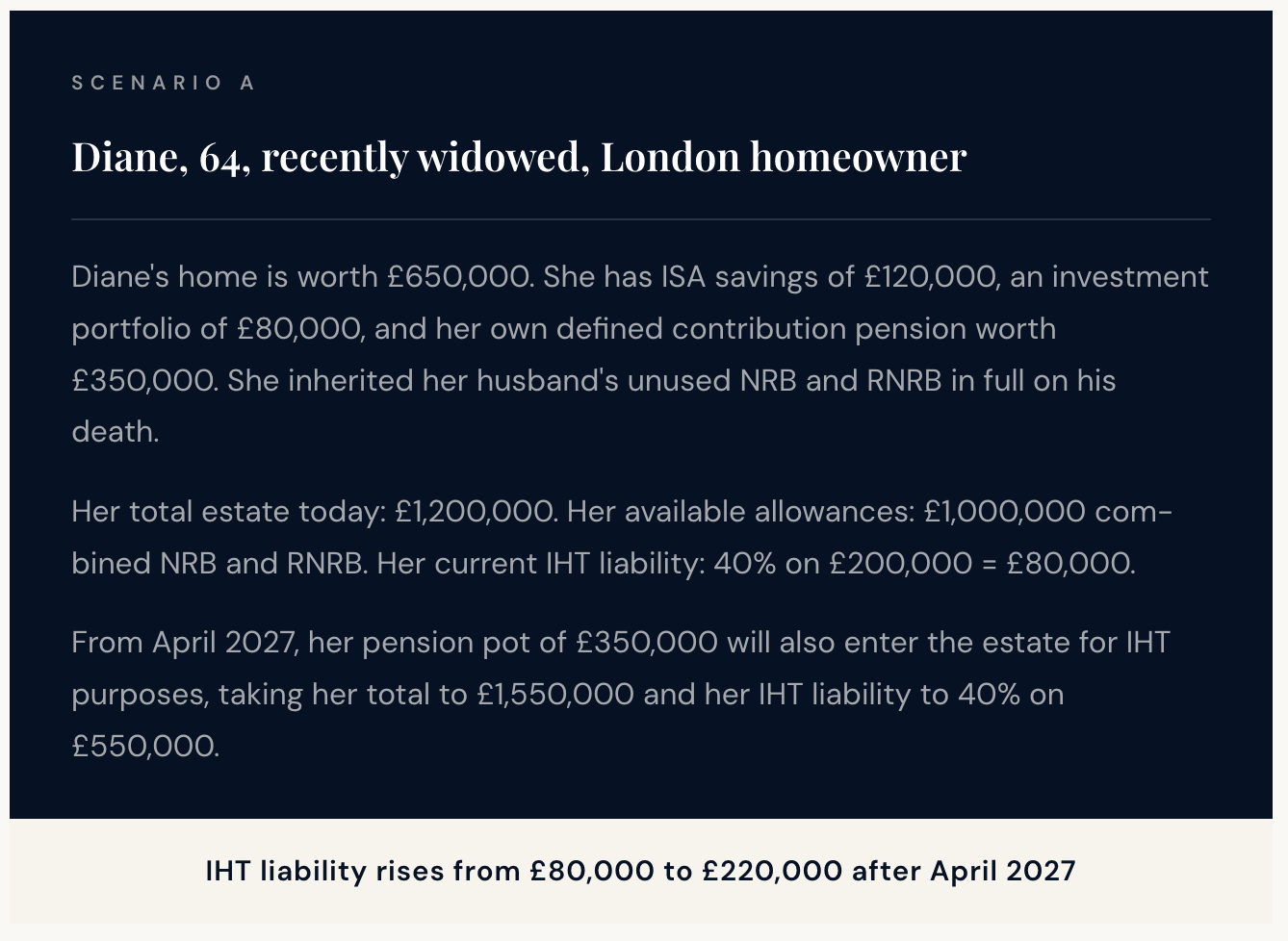

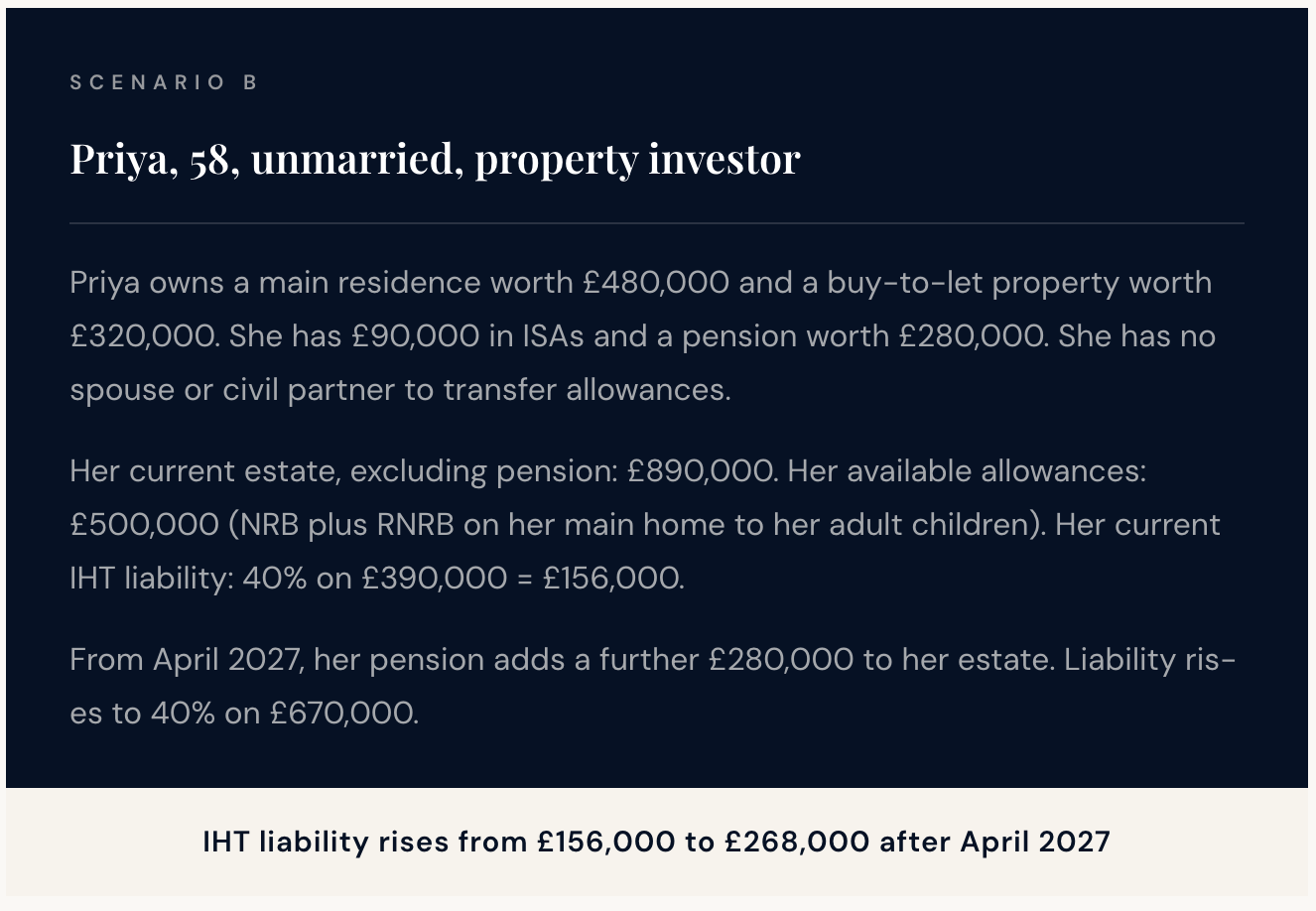

For professional women in their fifties and sixties, the risk is often more nuanced than the headline numbers suggest. A home bought in London or the South East twenty years ago may already be worth enough, combined with ISA savings and a defined contribution pension, to push a single person's estate toward or beyond the half-million threshold. Add an inherited pension from a late spouse, and the calculation shifts again.

"The nil-rate band has been frozen since 2009. House prices have roughly doubled. The government has raised a great deal of tax without technically raising the rate at all."

Office for Budget Responsibility · Spring Forecast 2026

The April 2027 Pension Change: What You Need to Understand

For decades, unused defined contribution pension pots sat outside the estate for inheritance tax purposes. The reason was structural: most pension schemes are set up as discretionary trusts, meaning that on death the money passes according to the scheme trustees' discretion rather than as a direct asset of the deceased. Because you never had an absolute entitlement to the funds, they were not counted as part of your estate.

The government's view, stated explicitly in its 2024 Budget documentation, is that pension freedoms introduced in 2015 and the abolition of the lifetime allowance transformed pensions from retirement savings vehicles into something more closely resembling inheritance planning vehicles. From 6 April 2027, that advantage disappears. Most unused pension funds and death benefits from registered schemes will be brought within the estate for IHT purposes, subject to 40% tax above available allowances.

There are some important nuances. Pensions passing to a surviving spouse or civil partner remain exempt, as do payments to registered charities. Annuities in payment and dependants' scheme pensions are also outside scope. But for the majority of defined contribution pension pots with named beneficiaries who are not a spouse, the change is significant and immediate in its planning implications.

The double taxation risk is also real and worth understanding. If a beneficiary inherits a pension and draws income from it, they pay income tax at their marginal rate on the withdrawals - up to 45% for additional-rate taxpayers. Stacked on top of the 40% IHT charge on the pot's value at death, the combined effective rate can reach 67% or higher for large pots passing to higher-rate taxpayers. This is not a theoretical risk. It is a planning consideration that advisers are already working through with clients.

Reducing Your Estate: What Actually Works

Effective IHT planning is not about finding loopholes. It is about using the allowances and reliefs the government has designed into the system deliberately, and using them early enough to make a meaningful difference. The strategies below are well-established, widely used, and entirely legitimate.

Gifting is the most powerful and the most time-sensitive tool available. Assets given away as outright gifts generally fall outside your estate after seven years, provided you survive the gift by that period. During the first seven years, a sliding scale of taper relief reduces the potential IHT charge. Gifts do not need to be large to make a difference over time: the annual gifting exemption of £3,000 per person, which can be carried forward one year if unused, provides an immediate and simple starting point. Gifts from surplus income, regular payments that do not affect your standard of living, are immediately exempt, with no seven-year waiting period, and remain significantly underused.

Trusts offer more sophisticated control over how and when wealth passes to beneficiaries. A well-structured trust can remove assets from your estate while allowing you to specify conditions of inheritance which are particularly useful where beneficiaries are young, or where you want to retain a degree of oversight over how wealth is used. Trust law is complex and the tax treatment varies considerably by trust type, so specialist advice is essential before proceeding.

Life insurance written in trust is a straightforward and often overlooked solution. A whole-of-life policy written in an appropriate trust pays out on death directly to the beneficiaries, outside the estate, providing liquidity to meet the IHT bill without the family needing to sell assets. The premiums themselves reduce the estate over time. For many people, this is the most practical way to manage a known IHT liability.

Charitable giving reduces the taxable estate directly and, if at least ten percent of the net estate is left to charity, reduces the IHT rate on the remainder from forty to thirty-six percent. For estates with significant charitable intentions, the arithmetic often makes giving more rather than less efficient from a tax perspective.

The Pension Rethink

The arrival of the April 2027 changes does not mean pensions lose their value as savings vehicles. During your lifetime, the tax advantages of pension saving remain compelling: contributions attract income tax relief, growth is tax-free within the wrapper, and you control the timing of drawdown. What changes is the sequencing logic of which assets to draw first in retirement.

Under the old rules, many financial planners advised drawing on ISAs, investments and other assets first in retirement, leaving the pension pot intact as an IHT-efficient legacy. That logic no longer holds for most people. From April 2027, drawing down your pension during your lifetime and spending or gifting the proceeds may be more tax-efficient than leaving a large pot to be taxed at forty percent on death, with income tax layered on top when beneficiaries make withdrawals.

Some retirees with larger pots are already exploring annuities as part of this rethink. Converting pension savings into a guaranteed lifetime income removes the pot from the estate and, if the income generated exceeds living costs, creates the possibility of making regular exempt gifts from surplus income. This is not a universal solution, and the right approach depends heavily on individual circumstances, but the direction of the strategic conversation has shifted.

Beneficiary nominations also warrant an urgent review. Many people completed a pension nomination form when they first joined a scheme and have not looked at it since. Nominations that made sense a decade ago may not reflect your current wishes or family structure, and the April 2027 changes may alter which beneficiary structure is most tax-efficient for your specific circumstances.

A Note for Women Specifically

IHT planning has particular dimensions for women that financial services has historically been slow to address. Women in the UK continue to outlive men by an average of four years, meaning they are statistically more likely to be the surviving spouse who inherits a partner's estate and allowances, and who must then navigate the planning decisions alone. The inheritance of a late spouse's NRB and RNRB is extremely valuable, up to £1 million in combined allowances, but it does not reduce itself automatically. It requires a formal claim and careful administration of the estate at death, which is often left to executors working under significant emotional and practical pressure.

Women are also more likely to have fragmented pension histories due to career breaks for caregiving, part-time working patterns, or divorce, which means their pension pots may be smaller but their overall estate may still trigger IHT through property and accumulated savings. The interaction between divorce settlements, inherited assets, and IHT thresholds is another area where specialist advice pays dividends and where generic planning guidance frequently falls short.

The conversation about inheritance is also one that many families avoid until it is too late to act with any real effect. Starting it early, with proper professional support, is among the most meaningful financial gifts one generation can give the next.

Your IHT Planning Checklist

Calculate your current estate value including property, ISAs, investments and, critically, your pension pot. The number may surprise you.

Review all pension beneficiary nominations. Update them to reflect your current wishes and family structure, and consider the post-April 2027 implications of who you nominate.

If you are married or in a civil partnership, confirm that your late spouse's unused NRB and RNRB have been formally transferred and claimed. This must be done correctly to preserve the full £1 million combined allowance.

Begin a structured gifting programme now. The annual £3,000 exemption, gifts from surplus income, and regular small gifts to children and grandchildren all reduce the estate over time with no seven-year wait on the exempted amounts.

Review your will. Many people have wills that are years out of date and no longer reflect their assets, family structure, or the current tax rules.

If your estate exceeds £2 million, take specialist advice on the RNRB taper. Gifting assets to bring the estate below the threshold can restore the residence nil-rate band and save up to £70,000 in tax.

Consider whether a whole-of-life insurance policy written in trust makes sense for your position. It provides liquidity for your beneficiaries to meet the IHT bill without selling assets.

Revisit your drawdown strategy. Drawing from your pension during retirement and spending or gifting the proceeds may now be more tax-efficient than leaving a large pot for beneficiaries to inherit.

Seek specialist independent advice before April 2027. The interaction of IHT, income tax on inherited pensions, and individual estate structures is genuinely complex. General guidance is a starting point, not a plan.

Sources: HMRC Inheritance Tax thresholds (GOV.UK, November 2025), Finance Act 2025, OBR Spring Economic and Fiscal Outlook March 2026, Burges Salmon IHT pension analysis (August 2025), Womble Bond Dickinson IHT pensions briefing, Royal London pension IHT guide (February 2025), Standard Life Adviser IHT Q&A (January 2026), Ascot Lloyd estate planning analysis. This article is for information only and does not constitute financial or legal advice. Pension and IHT legislation referenced is subject to parliamentary approval and may be subject to further revision before April 2027. Always seek qualified independent financial advice tailored to your circumstances.