Investor checklist | What the Spring Statement Means for Your Money

No new taxes were announced today. But the policies already on the books are reshaping mortgages, pensions, ISAs, and investment returns in ways that every saver needs to understand.

Rachel Reeves took pains to bill today's Spring Statement as a non-event, and on one level she succeeded. There were no surprise tax rises, no emergency fiscal pivots, no dramatic rewrites of the rules. But for savers and investors, the absence of new announcements does not mean the absence of consequence. A raft of changes announced in the October 2024 and Autumn 2025 Budgets are now either already in force or approaching fast, and the OBR's updated forecasts carry their own clear signals for mortgage holders, pension savers, ISA holders, and anyone with money in the markets.

Below is a plain-language breakdown of every development that matters, organised by topic, with a clear action checklist for each.

Mortgages & Property

Homeowners · Buyers · Landlords

No housing policy changes were announced today. The statement's significance for mortgage holders lies entirely in what the OBR forecasts imply for interest rates and house prices, and the shadow cast by Middle East tensions on that outlook.

Mortgage rates have fallen from 2023 peaks The Chancellor highlighted that Bank of England rate cuts have reduced costs on new fixed-rate deals. Rates remain elevated by historical standards but are significantly below their 2023 highs.

Middle East conflict threatens rate outlookThe OBR's forecasts were built before the Iran escalation. Rising oil prices could push inflation back up, cooling expectations for further Bank of England cuts and potentially pushing fixed-rate deals higher.

OBR expects mortgage rates to rise to 4.5% from 2027 onwardsDespite current easing, the OBR forecasts the average rate on mortgages will climb and hold at 4.5% per year from 2027 to 2030, above the current 4.1% baseline.

House prices forecast to rise steadily at 2.4–2.9% per yearThe OBR projects consistent nominal house price growth across the forecast period, offering some reassurance to existing owners but little comfort to first-time buyers.

Landlords face a two-percentage-point rise in property income tax from April 2027Already announced in the Autumn Budget, the increase in the rate of tax on property income will materially affect buy-to-let economics. Landlords should review portfolio yield calculations ahead of the change.

Action checklist: Mortgage & Property

If your fixed-rate deal expires in 2026, consider locking in a new rate up to six months early to avoid reverting to a Standard Variable Rate

Do not assume further rate cuts will be significant: the geopolitical situation means the Bank of England may pause its easing cycle

Landlords should model the April 2027 property income tax rise into their portfolio returns now and consider whether to restructure ownership

First-time buyers: the stable but elevated rate environment is unlikely to improve dramatically; affordability modelling now beats waiting

Pensions

Retirement savings · Inheritance · State pension

No new pension changes were announced today, which pension industry figures welcomed as a relief after a turbulent period of policy. However, the changes that are already locked in are significant, particularly for those using pension pots as part of estate planning.

No new pension changes announced todayT he Spring Statement contained zero pension policy announcements, which the industry broadly welcomed. The focus now shifts to the Autumn Budget 2026.

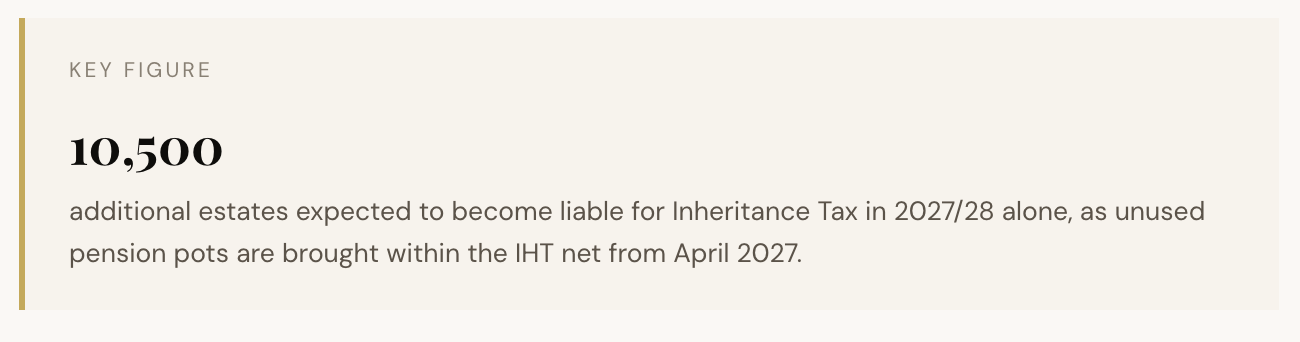

Inherited pension pots subject to IHT from April 2027 From April 2027, most unused pension benefits will be included in estate calculations for Inheritance Tax purposes. The OBR estimates this change alone will bring 10,500 more estates into IHT liability in 2027/28, rising to account for around 14% of total IHT receipts by 2030/31.

One million additional pensioners drawn into income tax by 2031 The OBR confirms that frozen income tax thresholds combined with the triple lock mechanism will pull around one million more pensioners into paying income tax by 2031. The Chancellor has indicated those whose sole income is the state pension will be exempt, but no formal mechanism for this has yet been published.

Salary sacrifice cap arrives in 2029 Restrictions on pension salary sacrifice contributions, announced previously, take effect in 2029. Higher earners using salary sacrifice as a significant tax-efficiency tool should factor this into long-run planning.

Frozen allowances continue to erode real pension tax relief value Income Tax thresholds remain frozen until April 2031, creating fiscal drag. Savers on rising incomes should review their pension contribution levels, as additional contributions can reduce exposure to higher-rate tax.

Action checklist: Pensions

Urgently reassess any estate planning strategy that relies on pension pots passing tax-free to beneficiaries: from April 2027, this no longer applies

Maximise annual and carry-forward pension contributions now to manage income tax exposure while relief remains available

If you are approaching retirement, seek independent advice on whether drawdown or annuity structures better suit your new IHT position

Review trust structures before April 2026 rule changes take effect on Agricultural and Business Property Relief

ISAs & Cash Savings

Cash ISA · Stocks & Shares ISA · Savings accounts

No changes to ISA rules were announced today and no further detail was given on the proposed cash ISA allowance reduction. The OBR's inflation forecast suggests savings rates may begin to ease, but the geopolitical risk now points in the other direction.

No new ISA changes in today's statement The ISA regime remains unchanged as of today. The proposed reduction of the cash ISA allowance was not confirmed, and no Lifetime ISA replacement was announced.

Cash ISA allowance reduction still in play for Autumn Budget The government has signalled its intention to reduce the cash ISA annual allowance from £20,000, with figures of £12,000 or lower having been publicly discussed. No date or confirmed figure has been given. Savers should maximise the current £20,000 allowance in the 2025/26 tax year before April.

Inflation falling to 2.3% may reduce the appeal of cash savings With inflation expected to fall toward the Bank of England's 2% target, the urgency of holding cash as an inflation hedge diminishes. However, today's energy price spike risk means this outlook could shift.

Personal Savings Allowance squeezed by frozen thresholds As more savers are pushed into higher-rate tax bands by frozen thresholds, the personal savings allowance halves from £1,000 to £500. Those at or near the higher-rate band should consider whether ISA wrappers are being used to their full advantage.

Energy bill savings of £150 per household from April The removal of green levies from household energy bills, confirmed and in force, will save the average household £150 per year and has been cited as the largest single driver of the improved inflation forecast.

Action checklist: ISAs & Savings

Use your full £20,000 cash ISA allowance before 5 April 2026: if the allowance is cut in autumn, what you have already sheltered is protected

Review whether a stocks and shares ISA now makes sense for longer-term savings given the government's clear preference for equity investment

Check whether frozen thresholds have moved you into a higher tax band, reducing your personal savings allowance to £500

Monitor Lifetime ISA developments: no replacement has been announced, but reform is expected before the Autumn Budget

Investments, CGT & Dividends

Equity investors · Business owners · Dividend income

This is the area where already-confirmed changes are most sharply felt. Dividend tax rates rise this April. Capital gains tax receipts are forecast to surge to 2030. Business owners with shares or investment portfolios need to act with some urgency.

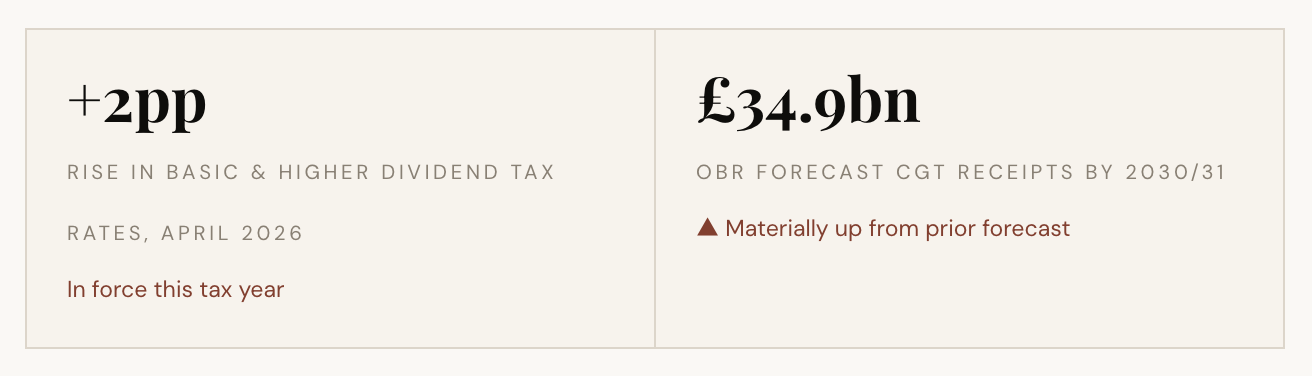

Dividend tax rates rise by two percentage points from April 2026 Both the basic and higher rates of dividend tax increase by two percentage points this month. This affects anyone receiving dividend income from company shares, investment trusts, or who pays themselves via dividends as a company director.

CGT receipts forecast to reach £34.9bn by 2030/31 The OBR projects Capital Gains Tax revenues will rise materially above prior forecasts, driven by rising equity prices and the changes to CGT rates introduced in the October 2024 Budget. Higher realised gains mean the government is watching this space closely.

Business Asset Disposal Relief under pressure With CGT revenues rising and the Autumn Budget approaching, Business Asset Disposal Relief remains a possible target for further tightening. Business owners planning a sale should not assume current rates will hold beyond October 2026.

Agricultural and Business Property Relief curbed from April 2026 The reform of APR and BPR, already announced, takes effect from April 2026. Family business owners and farmers should have already taken specialist advice on restructuring to limit the IHT impact.

Equities supported by improved macro outlook but Middle East risk is real The OBR's improved growth and inflation forecasts support risk assets in theory, but the market's focus on Iran and energy prices means sentiment may move faster than any economic forecast can track.

Action checklist: Investments & CGT

Ensure any dividend income is sheltered in an ISA where possible to avoid the April 2026 dividend tax rise

Company directors paying themselves via dividends should review their salary/dividend split now that rates have risen

Consider realising gains before further CGT tightening in the Autumn Budget; use your annual CGT exemption (£3,000) each tax year

If a business sale is planned within two years, seek advice on Business Asset Disposal Relief eligibility immediately

Family farming or business property owners must review APR/BPR structures before April 2026 rule changes bite

Income, Wages & Tax Thresholds

Employed savers · Higher earners · Fiscal drag

Frozen tax thresholds continue to pull more people into higher tax bands even as wages rise, a phenomenon economists call fiscal drag. The Chancellor offered no relief on this front today.

Income tax thresholds frozen until April 2031 The personal allowance (£12,570) and higher-rate threshold remain frozen until April 2031 in England, Wales, and Northern Ireland. With wages rising, more people are being drawn into higher-rate tax than would otherwise be the case.

National Living Wage rises by 4.1% in April 2026 Workers aged 21 and over see their minimum wage increase. This may have a secondary effect on employers' cost bases and pricing, noted by businesses as a live concern.

Household disposable income forecast to grow at twice the autumn projection The Chancellor pointed to OBR data showing real household disposable incomes are now expected to grow faster than previously forecast, leaving the average person around £1,000 better off annually by the next election. Per capita GDP growth of 5.6% is expected across the parliament.

IHT nil-rate bands also frozen until April 2031 The Inheritance Tax nil-rate band (£325,000) and residence nil-rate band (£175,000) remain frozen, meaning more estates will be caught as house prices and asset values rise.

Action checklist: Income & Thresholds

Check your current tax code: workers who have moved jobs or received pay rises may be on incorrect codes and overpaying

Married couples should consider using the Marriage Allowance to transfer up to £1,260 of the personal allowance to the higher-earning partner

Higher earners should maximise pension contributions to bring taxable income below the £50,270 higher-rate threshold where possible

Review your estate and begin gifting strategies to reduce IHT exposure while nil-rate bands remain frozen through to 2031

Key figures from the OBR's Spring Forecast 2026

GDP growth 2026: 1.1% (revised from 1.4%) · GDP growth 2027–28: 1.6% · CPI inflation 2026: 2.3% · Unemployment peak 2026: 5.3%, falling to 4.1% by 2030 · Public sector net borrowing: falling from 4.3% of GDP this year to 1.8% in 2029–30 · Fiscal headroom: £23.6bn against self-imposed borrowing rules · GDP per person growth over this parliament: 5.6%

Sources and notes: All figures are drawn from the OBR Economic and Fiscal Outlook, March 2026, and from the Chancellor's Spring Statement address to the House of Commons, 3 March 2026. The OBR explicitly notes that forecasts do not incorporate any economic impact from the ongoing Middle East conflict and are subject to revision. This briefing is informational only and does not constitute financial advice. Consult a qualified financial adviser before making changes to your savings, pension, or investment strategy.